(Here is the updated version of my research on this company: link)

Coffee is a very sticky category. They become your habit and gets inside your daily routine. Sometimes, if you don’t get a good cup of coffee in the morning your whole mood gets spoiled for the day. So, changing this habit can be quite difficult.

Thinking about the point mentioned above I started analysis of a company called CCL Products (India) Ltd.

About

CCL Products (India) Ltd was formed set up in 1994 and commenced commercial operations in 1995. It is an export oriented unit with the ability to import green coffee into India from any part of the world and export the same to any part of the world, at cost advantage like with no/less duties due to benefits received by trade agreements between nations.

Business Model

Continental Coffee Limited Products India deals in two segment B2B and B2C.

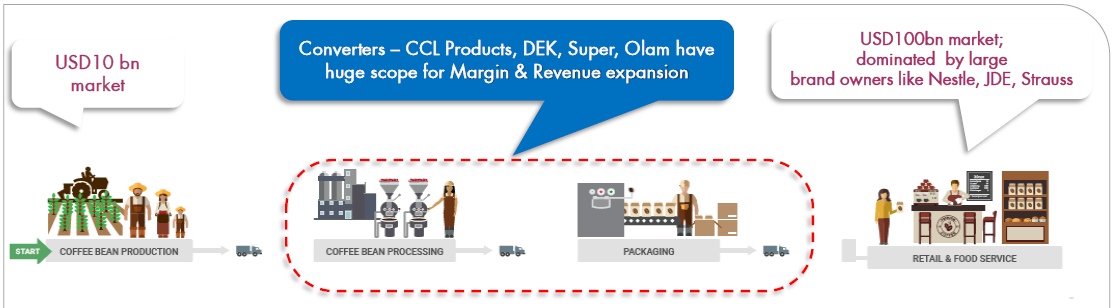

Here is an image to explain their B2B segment:

Source: Axis Securities

So, as the image above shows CCL Products (India) Ltd is in processing business. They buy raw material and process the coffee beans and then export it to their customers.

Company does not own any coffee plantations instead they procure green coffee from Chikmagalur in Karnataka, India as well as imports premium variety like Robusta and Arabica from Vietnam and Ethiopia respectively and then does the processing.

The company works at cost-plus business model. They do not stock any raw-materials and places the order for the same only after getting an order for coffee, this protects them from coffee price fluctuations.

Further, CCL Products (India) Ltd has now also entered into consumer business.

They have launched their own consumer brand, Continental Coffee and plans to take it slowly instead of rushing it like they did in 1997.

In 1997, they had only one plain vanilla product therefore they had no USP which led to quite a bad experience. Company had to withdrawn there product due to bad response. Company was new to consumer market that time. They had done a nationwide launch of the product without understanding of the Indian market, which led to the failure.

But now they have entered the market after 20 years with the understanding of the market and taking things slowly to check the response. For example: company currently deals in South India market only and plans to expand on after gaining 5% market share.

Moat

- Stickiness of business: It becomes quite difficult for a company to switch to a different supplier when quality is big importance for them. So, businesses tend to ‘stick’ with the same supplier (CCL) which gives supplier power to charge high price. As getting the right blend in coffee is quite a task.Their customers would want to maintain consistency in quality and taste of their product which means they won’t go changing vendors easily therefore, this also creates hence switching costs barrier.

- As CCL Products (India) Ltd is one of the largest instant coffee producers in the world, it also gets a Moat of Economies of Scale due to its cost efficiency.Once company had lost a customer who had set up their own plant . But soon that customer had to return back as CCL’s price was lower than that customer’s cost. Plus that customer could not replicate the premium blend made by CCL. Thus this shows the power of CCL Products (India) Ltd.

- This is the only company in the world which is offering all four types of soluble coffee from one location. This means customers would prefer CCL as it would save them logistical costs. Also, with now having packaging capacity their Moat would start getting wider.

- Company’s customers have been with it for more than 15-20 years which shows that company has build good relations with them. Such relations require being updated with technology, trust, timely delivery and quality.

- CCL keeps the blend confidential. CCL has around 1000 different blends and catering to over 90 countries currently. These blends requires substantial R&D investment, thus not easily replicable.

- CCL Products (India) Ltd clientele is also their Moat:

- Jacobs Douwe Egberts (JDE), Strauss Coffee, & LMZ Soluble Coffee are some big brand to whom CCL supplies.

- Reliance Kaffe sold at Reliance outlets is manufactured by CCL and we can expect that in coming years we are going to see a retail boom which will be led by Reliance.

- They also supply to Dmart, Spencer, Big Bazaar, & D’aromas

- Their clients also include Amul and Lottee

- As they do not stock any raw materials and places order for the same only after getting a confirmation from customers this helps them in sustaining their margins.

- Having a plant in Vietnam helps company in having continuous availability to raw material (as Vietnam has ample amount of coffee raw materials). This also means low inventory requirement.

- The company has now shifted their focus from selling bulk generic products to small pack products which are ‘sticky’ as there are specialized as per the requirement. Currently 60% of their customers are loyal ones who go for specialized products.But why would their existing customer ask for small pack from them? If a customer takes small packs order from CCL the customer would also get cost advantage as their would be no middleman. Earlier CCL used to process the coffee and then export it to various location from there the coffee used to be transported to the customer after getting packed in small packages but now all this can be done from one location!

- They expand only after the demand. Like they did recently. Only the new plant in Chitoor is under debt and rest are debt free. So, currently the company focuses on clearly off debt.

- Management thinks that their current margins are sustainable due to their new freeze dry capacity, better technology, & new processes which are helping them get better yield.

- Company has built such strong relations that they also take advise from their customers on how to build their facilities so that it caters to customer’s demand.

- Company has recently crack into USA market which will lead to doubling of their revenues in USA. It took them 3-4 years to get the approval. This creates an enter barrier for competitors as they can’t one fine day decide to enter USA market.

- Comparing with competition both the players (Nescafe & Bru) the advantage which CCL has is economies of scale. CCL has double production capacity, which means per kg cost is going to be lower than the competition.

- The company saves cost on transportation with regard to India as they receive exemption of income tax from Vietnam. Also, Vietnam enjoy MFN status with many countries which helps the company save cost.

Nescafe & Bru vs Continental Coffee

- With my research I came to know that people liked the taste of Continental Coffee better than Nescafe (Remember this is very subjective and can be wrong). I think it is because CCL makes granules coffee which retains the aroma whereas Nescafe deals in powder coffee.

- In India, Nestle is into the business of selling agglomerated form of coffee and Bru sells Spray Dried powder which is in chicory blend. Whereas, CCL has made a new category which is agglomerated Spray-Dried coffee.

- Comparing with competition both the players (Nescafe & Bru) the advantage which CCL has is economies of scale. CCL has double production capacity, which means per kg cost is going to be lower than the competition [As mentioned above].

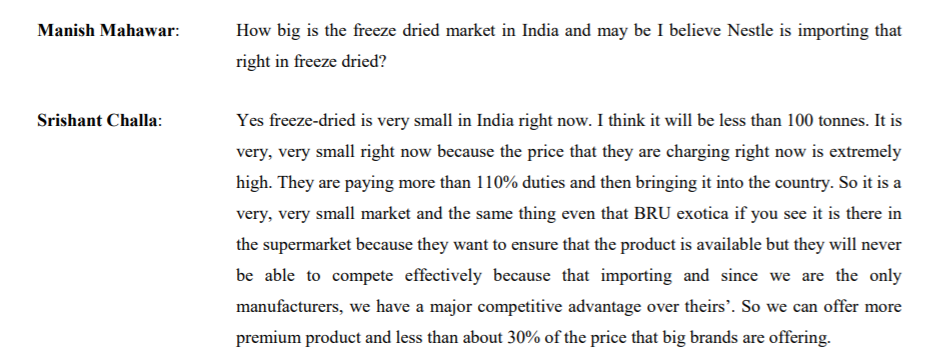

- In Q1 FY17 the management explained their competition with Nestle with regard to the Frezee Dried Coffee (look at the image below).Nestle has to pay 110% of import duties to bring in Freeze Dried Coffee whereas CCL Products (India) Ltd can sell the same at 30% less cost.

Tata Coffee Vs Continental Coffee

- In 2017, Tata coffee has build 5000 mt of freeze dried capacity in Vietnam due to incentives given by the government. I am not sure but I read somewhere that the incentives end in 2020 (Will update as soon as I find a reliable source).

- CCL Products (India) Ltd has more capacity than Tata Coffee, that is one of the reasons why CCL used to trade at higher multiples.

- Tata is also into the business of plantations, that is backward integration, which exposes them to risks like volatility in prices and productivity due to monsoon. So we can say that business models of Tata coffee and CCL Products (India) Ltd are different.

How the company keeps away the competition

There is lots of competition as there is lots of excess capacity in world. There is competition from Brazil, Mexico, Singapore, Malaysia, China, Vietnam, India, Europe.

But CCL Products (India) Ltd has still maintained its good position. The reasons being:

- Company has been maintaining strong customer relationship for over 20 years.

- CCL takes advantage of ASEAN agreement which protects company from competition coming from Brazil as importing from there could cost 9% of duties. Further for EU market India & Vietnam has 3.1% duties whereas Brazil has same 9% even here also. But we need to remember if a brand wants generic vanilla coffee Brazil would be their first choice but if they want specific quality then CCL comes into the play.

- They have created unique blends for customers and such blends are exclusive in that region and such composition is not revealed to customer also.

- In the initial years company had only 4-5 blends but now with investment in R&D they have over 1000 blends.

- Customers are usually very picky and they will stick with same quality standards. Therefore, once a customer introduces a particular blend into the market it is difficult for them to switch to other blends.

- Company also supplies coffee exclusively to military.

Growth Opportunities

- There is going to be expansion in Vietnam of around 3500 tons capacity.

- Management has said that their branded business is growing at 40% rate, which is sustainable.

- Company’s domestic team keeps on complaining that they are not delivered with enough stocks as demand keeps on rising. I think this is a good problem to have.

- There is huge growth opportunity in India as the consumption of is only 20,000 tons compared to Japan at 35,000 and USA at 80,000 tons. A positive change in consumer lifestyle (specifically driven by western culture) with increasing higher disposable income.

- USA has implemented FSMA law in 2020 which will stop import of low quality products. Fearing this some USA customers have already started to come to CCL as they are known for their quality.

- Large retail businesses in Switzerland don’t depend on one supplier, instead they keep minimum five suppliers with them. Therefore, this provides opportunity for CCL as to be one of the five suppliers.

- Growing number of young professionals: Instant coffee offers convenience in preparation, shelf life, which increases its demand among the urban consumers.

- Newer capacity coming up in Chitoor at FY18 which is high margin freeze dried capacity.

- Retail sales will start contribute meaningfully from FY19 onwards. Company focusing on brand building activity and forming distribution channel. As per management comment they are going step by step in this foray.

- USA is big opportunity for CCL products. Demand for instant coffee is 75000 ton USA alone. Currently CCL is supplying 2000 ton only.

- In 2018, one of the largest conglomerated and packing units in USA had shut down due to which their customers are not looking for supplier. This has created opportunity for CCL.

- In their earnings call of Q3 FY18 management had stated that they might plan to enter filter coffee in future (roasted coffee) and currently the market is of 1,000 cr.

- Further they also said that they plan to target 1-2 big customers every year on recurring basis.

- Their existing customers keeps on increasing their volume and also when a new customer is added first year the customer order basic vanilla product and then from second or third year after gaining trust they switch you more premium products, which leads to growth of 50-60% in volumes.

- CCL Products (India) Ltd by just installing few equipments can increase their Vietnam capacity by 15,000 MT and 5000 MT in India.

- Finally coffee is the second most traded commodity in the world after oil. Also, we know that caffeine is addictive so this gives us broader view that demand will be there.

About the Management

In Prof. Sanjay Bakshi’s article, Seven Intelligent Fanatics from India, he inverts the management analysis and gives four elements of dumb behavior which are as follows:

- Over-aggression, usually expressed in the form of excessive leverage;

- Growth without any regard to profitability;

- A tendency to gamble; and

- An inability or unwillingness to delegate, constraining growth potential.

Regarding the first point company has taken debt for their SEZ plant only and rest of their all plants are debt free. This shows that debt is for excessive.

Second point can be covered by noticing that company is not carefully expanding their B2C unlike their actions in 1997. Currently then only operate in south India and plans to expand only after gaining 5% market share.

Further, they had declined Joythy Labs offer to make new products as they were at full capacity. They could have taken debt and expanded but that would have been an unwise move. As the company only expands if there is demand. There was no guarantee of repeat orders or any new demand.

For the third point we can see that company’s core business is related to coffee and they deal in products related to that only. So, I think there are no signs of ‘DIWORSEFICATION’.

Forth point deals with ability to delegate. There is not such information regarding that but I believe they have a team which is handling their domestic business.

Updates

- Company has seen delay in delivery of stocks due to break of their delivery system due to COVID.

- There has been increase in employee cost as a new unit has been set-up.

- Company has strong business in Vietnam, which is not affected due to less number of cases in the country. This is the reason revenue did not drop severely.

- Currently the company has cleared its march inventory and their production level is back to normal.

- Due to this pandemic retail demand has increased but institutional demand has fallen. So, that gets nullified.

- Vietnam unit gets tax benefit which is not for lifetime!

- Currently, their market share in South India is 4%. Management says that as soon as they reach 5% they would start entering new market and plans for the same has already began. The reason for taking things slowly is due to their past experience of 1997. In 1997, company had decided to enter retail business and launched their nationwide. They had only one plain vanilla product and experience was so bad that they had to withdrawn there product. But now after researching and bringing in specialized products they entered the market after 20 years!

Threats

- CCL Products (India) Ltd avoids commodity risk by having contracts on a back to back basis at fixed prices.

- Further, currency risk is also avoided as entire coffee trade is USD denominated

- There can be huge risk of bad debts as this company has concentrated clients. But looking at the past records and their relations even such risk is avoided till an extend.

- Tata Coffee has build 5000 mt of freeze dried capacity in Vietnam. This is small capacity but this shows they have entered into the league.

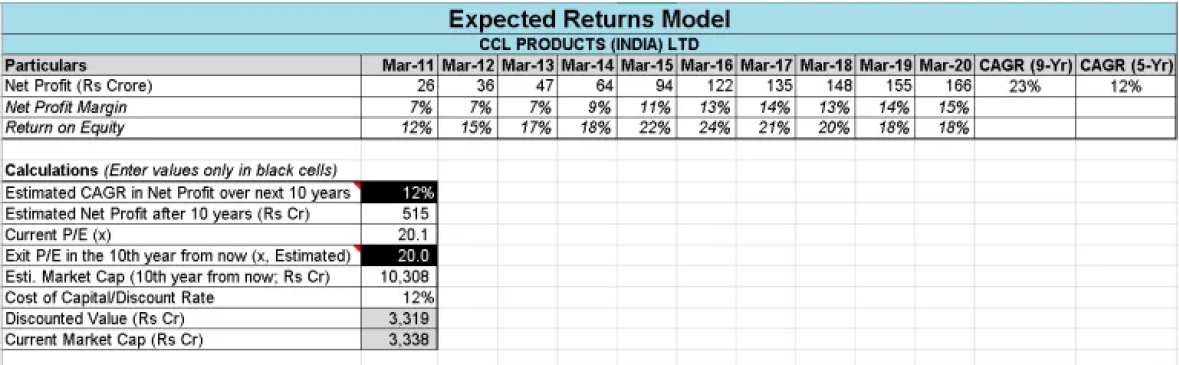

Valuation

I try to follow the expected return model which is followed by Prof. Sanjay Bakshi. Here is the link to it: (click here)

Its a three step process:

- It must be a business with a Moat

- Taking conservative assumption of performance

- Following uniform exit multiple of 20x for all such businesses as a discipline.

As said by Prof. Sanjay Bakshi such practice provides margin of safety by:

“The idea behind the above is to create multiple sources of margin of safety. The first point delivers a margin of safety by keeping you away from bad businesses. Investors should recognize that margin of safety, apart from a low price, can also come from a high-quality business. The other two points help you think about reasonable valuation a decade from now.“

This valuation is made further simpler by using an excel sheet (provided by Safal Niveshak, thanks to him!):

Remember depending completely on Excel can be quite dangerous sometimes. As people tend to tweak it as per their needs.

What I follow is after my thorough analysis I just put in the numbers in the excel sheet and if the market cap is near the discounted value I would buy shares of the company.

Inshort

CCL Products (India) Ltd has a cost-efficient business model, long-standing relationships with customers as the product has stickiness, economies of scale as they are the lowest cost producer, they have the expertise to produce the right blends and their location which saves them logistical costs helps the company get an edge over competitors.

——

Sources: Annual Reports, Conference Calls & as cited during the article.

Disclaimer: I am not a SEBI registered adviser. All the information provided by me are for educational/informational purposes only.